Data center buildout is accelerating – and so is energy demand

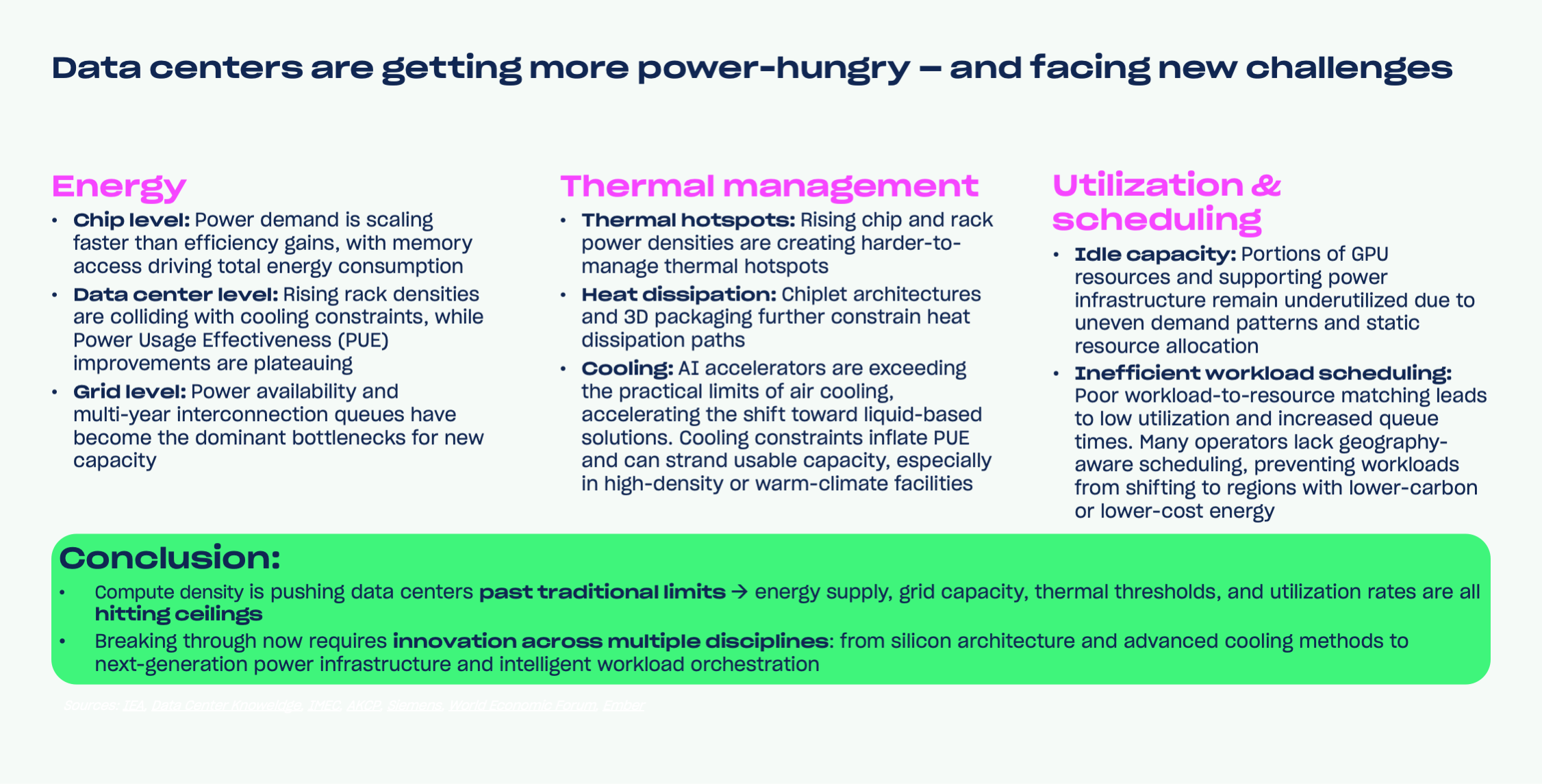

The global expansion of data centers is accelerating at a breathtaking pace. Meeting the surging demand for compute power is expected to require an estimated $6.7Tn in data center infrastructure and power investment by 2030. This growth is driving a sharp rise in energy consumption. Data centers are projected to consume 500-600 TWh in 2026, roughly 2% of global electricity demand and already comparable to Germany’s total annual consumption. By 2030, this is expected to nearly double to around 1,000 TWh.

A major driver of this surge is AI. Today, AI workloads account for approximately 15% of total data center energy use, and that share is rising quickly. The impacts are especially acute at the local level: grid constraints and infrastructure bottlenecks are creating serious energy challenges, with electricity prices increasing by as much as 267% near major data center clusters. Regionally, the United States clearly leads, accounting for about 45% of global data center electricity consumption, while Europe represents roughly 15%.

These emissions are closely linked to the carbon intensity of local grids, which in the near term remain dominated by fossil fuels. Data center CO₂ emissions are expected to increase from about 220MtCO₂ today to 320-500MtCO₂ by 2030. Adding to the urgency, major tech firms may be underreporting data center emissions by as much as 662%, raising serious questions about whether Big Tech can achieve their climate commitments.

Sources: IEA, The Guardian, CNN, Bloomberg, Ember, McKinsey

Europe’s trajectory – defined by energy, regulation, and sovereignty

The expansion of data centers across Europe is being held back by a number of structural constraints, including limited access to competitive, low-carbon power, increasing grid congestion, lengthy interconnection lead times, and a fragmented landscape of energy policies, permitting regimes and approval processes. These factors collectively impede both grid connection and site development.

However, several powerful trends are converging. European governments are tightening rules to retain control over data, infrastructure, and critical digital services, while European companies increasingly view sovereignty as a core criterion for where data is stored and how infrastructure is operated. This is accelerating adoption of local inference and federated architectures, and is contributing to a broader build‑out of data centers across the continent.

Stricter sustainability requirements are also emerging. The EU’s Energy Efficiency Directive will mandate more granular energy reporting and push data centers toward carbon neutrality.

On the investment side, the EU’s InvestAI program aims to mobilize €200Bnfor AI and its infrastructure, including a dedicated €20Bn fund for AI gigafactories, large hyperscale data centers intended to anchor Europe’s compute sovereignty.

Sources: IEA, Ember, Data Centre & Network News, CERRE, EUDCA, Bundesregierung, European Commission

Value chain – Overview

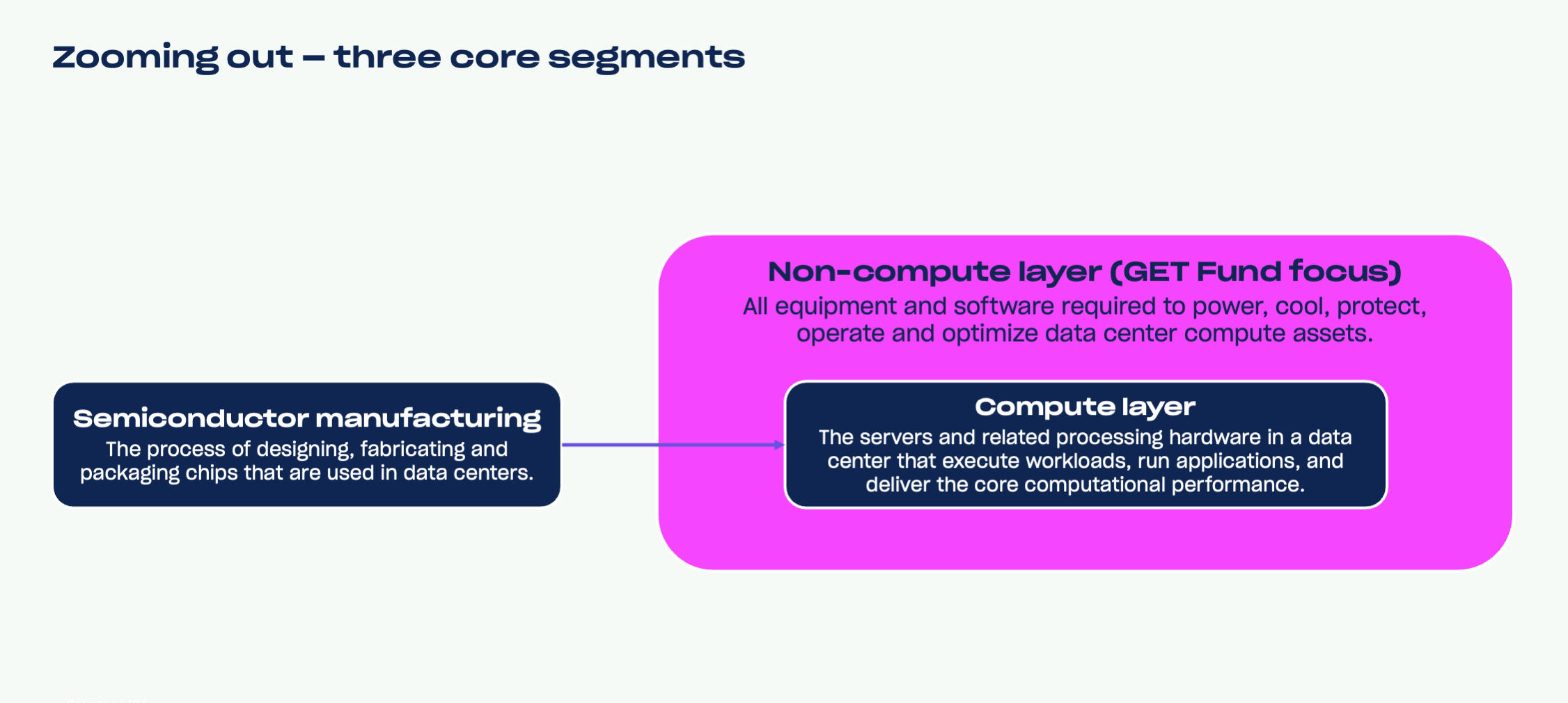

Mapping the data center value chain, we identified three core segments:

GET Fund investment focus

Semiconductor manufacturing and the compute layer fall outside of GET Fund’s focus. These sectors are characterized by long development cycles, significant capital requirements, and high barriers to entry, dynamics that are difficult to reconcile with our investment thesis.

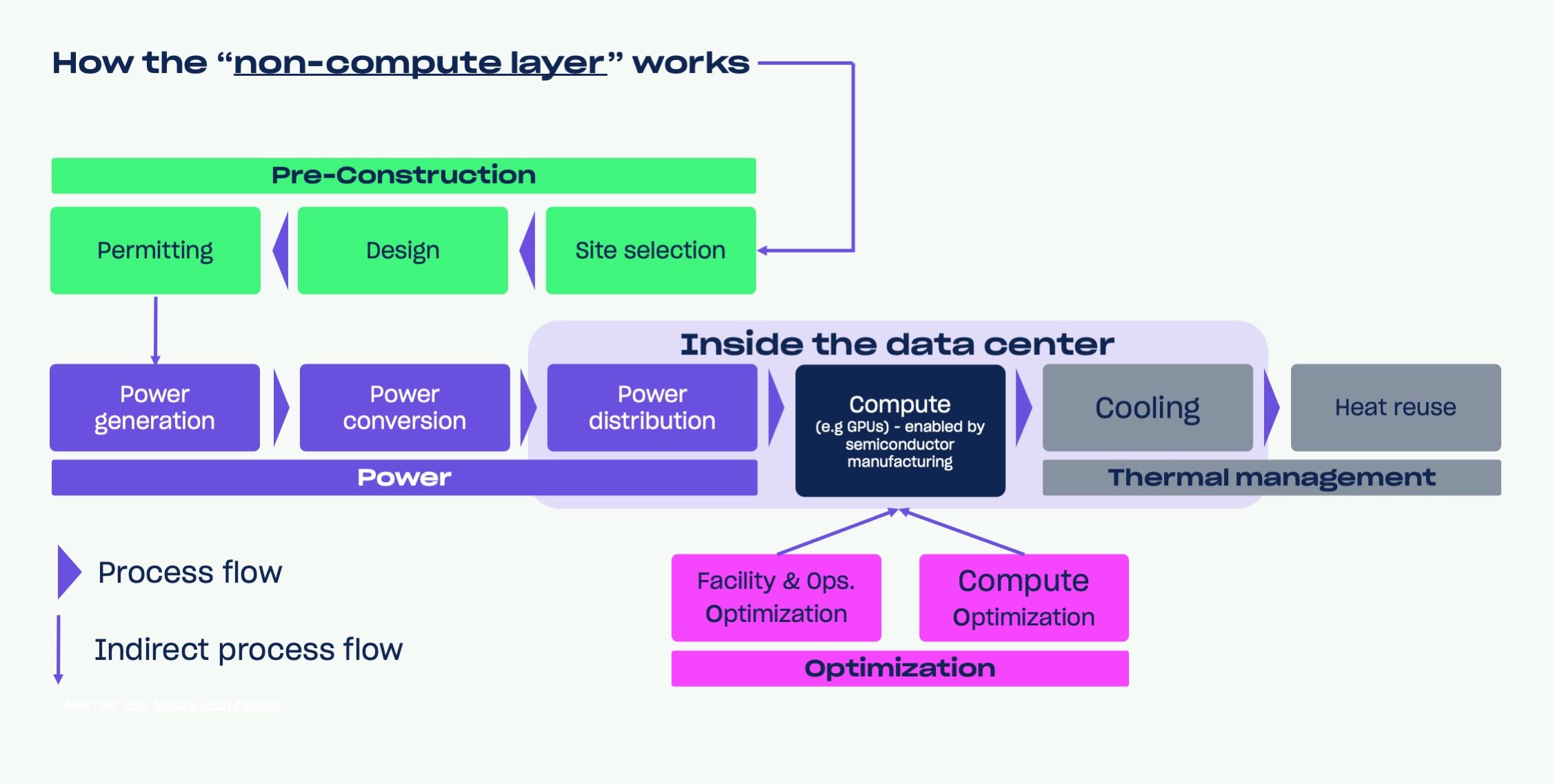

Our focus is the non-compute layer of the data center stack, encompassing the equipment and software required to power, cool, protect, operate, and optimize data center compute assets. Depending on the data center type, the non-compute layer accounts for 20-40% of lifecycle energy demand, making it a critical lever for improving efficiency and reducing the environmental footprint of data center operations.

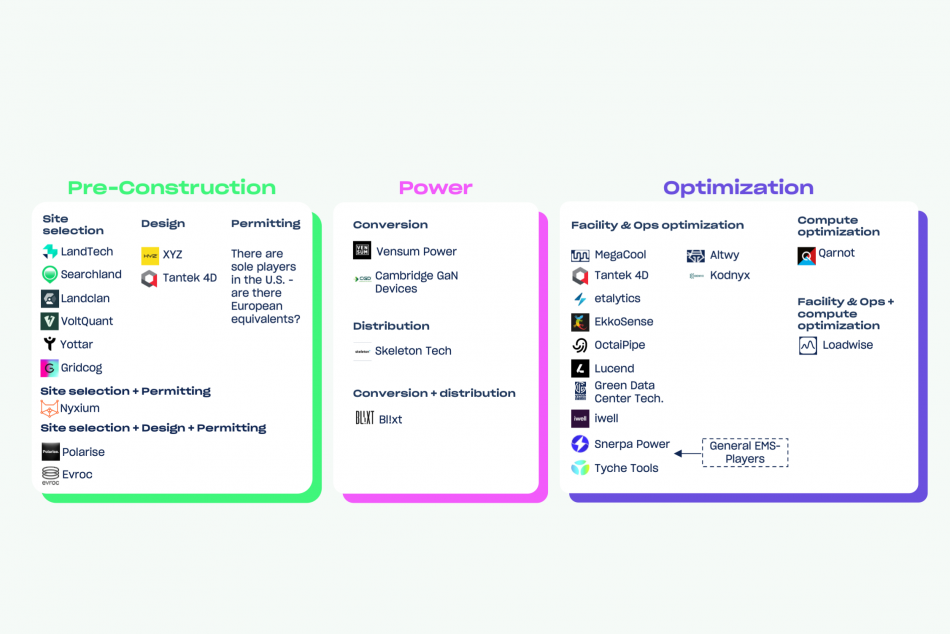

We mapped the full non-compute landscape (see picture) and, within this layer, identified the following priority categories (see outlined boxes).

We target the non-compute layer because it includes a rich set of integrated hardware-software and pure software technologies, characterized by faster development cycles, lower barriers to entry, and generally higher technology readiness levels than other segments of the data center stack.

Power generation and thermal management (cooling and heat reuse), however, fall outside our priority categories. Relative to our focus areas, these technologies tend to be more capex-intensive and hardware-heavy, carry longer project timelines, and present structurally higher barriers to entry.

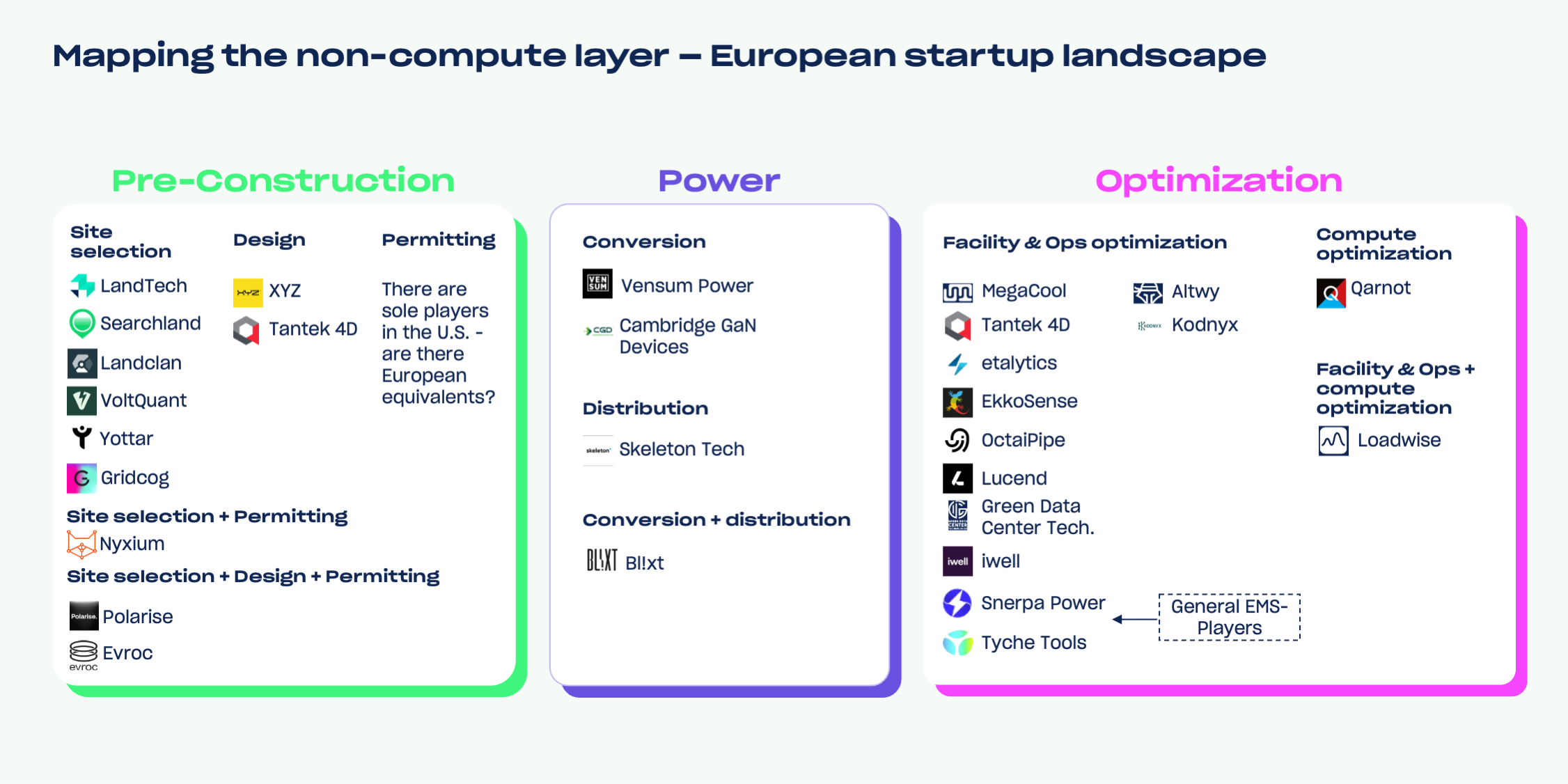

Below, we present the European startup landscape across our focus areas:

If you are building technology in this space, we would love to hear from you.

Reach out to us to explore how we can support your journey or pitch us your startup.

Back to Insights