Waste management looks deceptively simple from the outside: a bin, a pickup, a treatment site.

In reality, it’s a complex, fragmented value chain with many stakeholders and handovers, spanning waste generators, facility managers, haulers, brokers, transfer stations, sorting facilities, recyclers, incinerators, landfills, and regulators. Each handover is a point where information degrades, incentives diverge, and responsibility shifts. This fragmentation makes existing processes in the waste management value chain inefficient, outdated and expensive.

The cost of waste

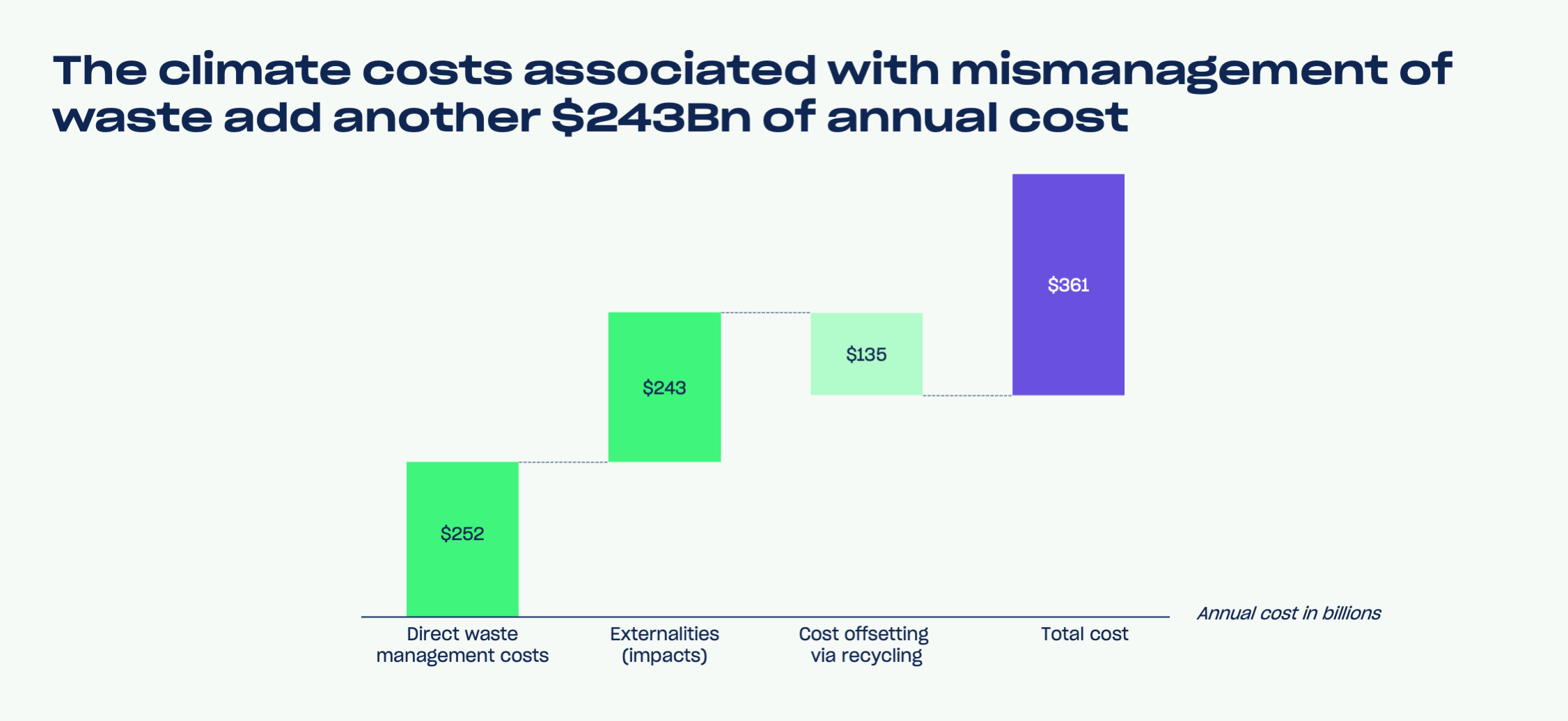

Managing municipal waste alone causes $252Bn worth of direct costs per year globally. Additionally, the financial cost of environmental harm adds another $243Bn per year. Increasing recycling rates can offset 28% of the bill, however, this assumes government intervention and significant investment in infrastructure. Even with significant progress in recycling, the direct cost associated with waste management is expected to reach $394Bn by 2050 (IWSA, Global Waste Management Outlook 2024).

Controlling these costs is crucial to reduce the financial burden on public authorities, and the environmental impact. This provides opportunities for new cleantech solutions that optimise the value chain. Where are the biggest levers?

One of the clearest takeaways from our recent deep dive is that lack of oversight into waste type and composition creates an uncertainty premium both for waste generators and processors. In simple terms: the lack of waste oversight is expensive.

Waste is priced and processed differently depending on many factors, such as type and contamination level. However, in many real-world settings, composition is poorly measured or not measured at all, especially once waste is aggregated across sites, containers, or routes. When stakeholders can’t reliably answer “what’s in here?”, they default to assumptions that protect them from downside risk. Those assumptions translate into buffers, extra handling, more exceptions, ultimately driving up costs.

For waste haulers, “unknown composition” is operationally expensive. Route planning and asset utilization become less efficient when loads are unpredictable; the fixed-cost model means inefficiencies quickly hit margins. Exceptions become more frequent: reclassification, rejected loads, extra sorting, additional documentation, and the inevitable back-and-forth between parties when something doesn’t match what was expected. Over time, this uncertainty gets baked into the commercial model. While haulers may absorb some of the cost in the short term, the uncertainty and risk of opaque waste streams get priced into contracts, thus passed through to waste generators.

Waste generators, especially commercial customers, feel this in two ways. First, directly, through cost leakage: paying for the wrong service level (container sizing, pickup frequency), paying “mixed/unknown” pricing because streams aren’t clearly separated, and getting hit with reclassification or contamination-related charges. Second, indirectly, by losing the very levers that would give them leverage to negotiate their contracts. If you can’t see the composition of your waste, you can’t pinpoint where it originates, what’s driving contamination, or which intervention would actually reduce cost or risk. Waste turns into a passive overhead instead of a manageable operational category.

Aligning incentives and defining the business case

Comparing recycling and landfill costs adds an important (and slightly uncomfortable) dimension to this story: landfill is often still cheaper than recycling. As a result, there are few incentives for waste haulers to work toward better sorting and transparency just because it’s environmentally preferable. If the lowest immediate-cost path is disposal, then voluntary investment in measurement and separation can stall.

The sales pitch cannot be “we make more money by recycling more.” Waste intelligence creates value through control and predictability: fewer exceptions, fewer disputes, clearer contracting, better service design, and lower cost volatility. It also creates resilience against change. When regulations tighten, landfill pricing shifts, reporting requirements expand, or customers demand evidence, operators with transparent data will adapt faster and with fewer surprises.

Investment opportunities

Our market research showed that circular economy startup activity is highly concentrated upstream, with the majority focusing on front-end interventions like biodegradable inputs, and new materials and packaging. Recycling shows the second largest area of startup activity. As a result, VC funding predominantly flowed into capex-heavy solutions with unclear go-to-market times and unit economics, limiting their ability to scale and make a real impact in the industry.

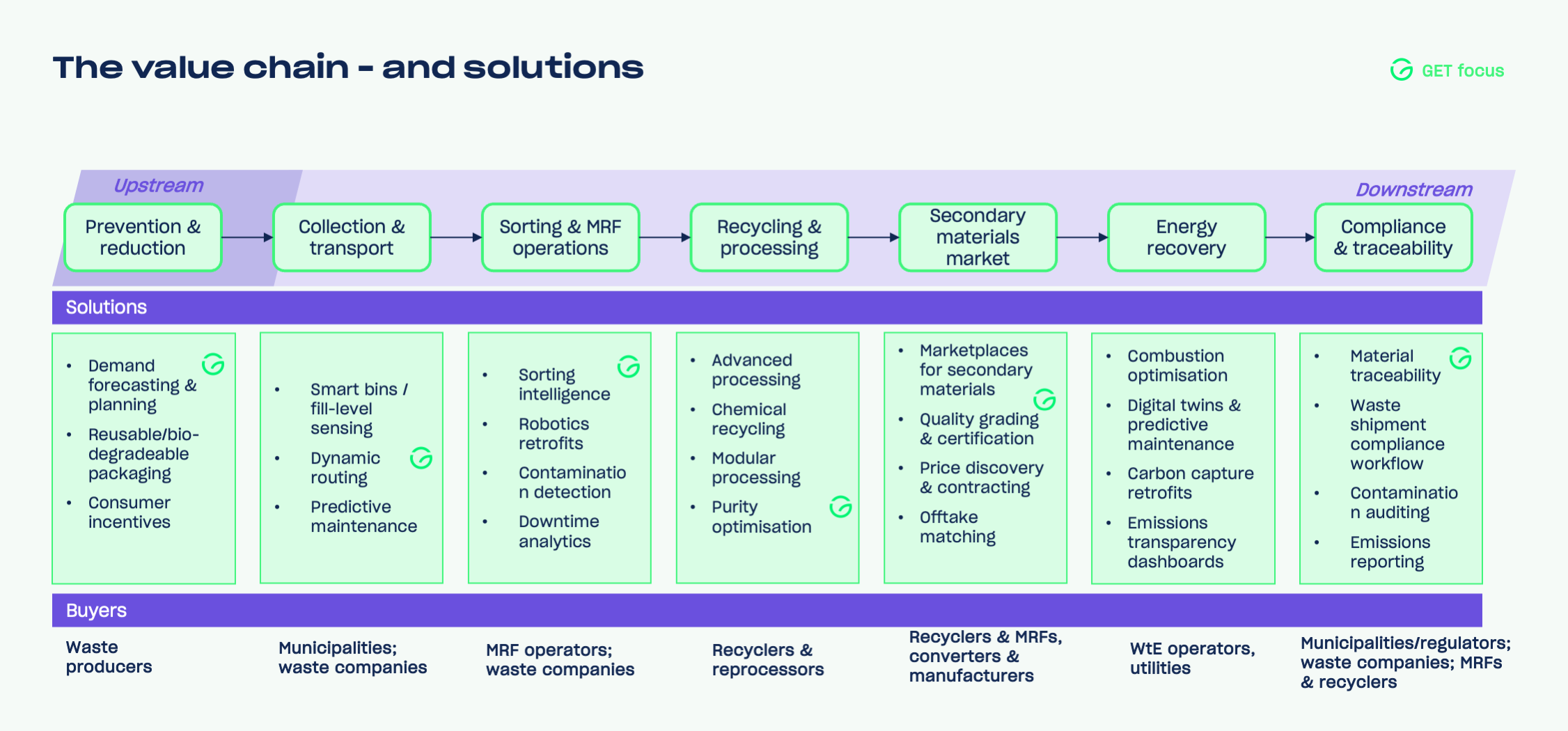

This creates whitespace for companies building the systems layer: tools that make waste measurable, auditable, and operationally optimizable across handovers. AI has opened new opportunities to turn fragmented, manual processes into scalable workflows. We are tracking solutions for accelerated waste profiling (auto-classifying streams, flagging contamination in real time, translating audits into operational actions), cost intelligence (invoice reconciliation, anomaly detection, benchmark pricing to improve negotiation power), and proactive planning through more dynamic forecasting and routing decisions.

This is what we are most excited about at GET Fund. Waste is a physical, regulated, multi-stakeholder system; exactly the kind of environment where a strong data and workflow layer can have outsized impact. We focus on scalable business models that decarbonise infrastructure-heavy sectors. For waste management, this means reducing friction in a fragmented chain and turning waste management from a reactive service into an optimisable operational system.

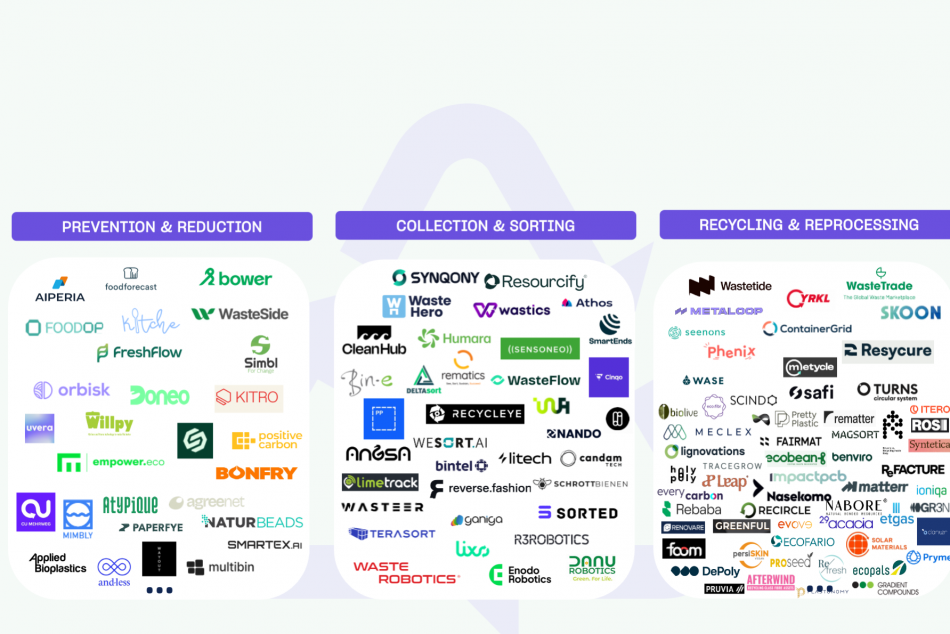

GET Fund market map

Below, you can see our startup map with (some of the) key European players. Who are we missing? Let us know in the comments!

Back to Insights