At GET Fund, we invest in founders who build the infrastructure for a zero-carbon economy. Electric vehicle charging has emerged as one of the most dynamic, yet most complex parts of that transition.

The early story was simple: more electric vehicles need more chargers. The market has now matured. Billions have gone into rollout, and coverage across Europe and other key regions are catching up. The challenge ahead is not about building faster. It is about making what already exists more reliable, integrated, and profitable.

Utilization rates are improving but still vary widely by region and site type. Grid connections and permitting can take several months, sometimes even years. The result is a market that is growing quickly in physical scale, but uneven in financial performance. The real opportunity now lies in software, data, and integration — in the intelligence that turns infrastructure into a sustainable business.

Market reality check

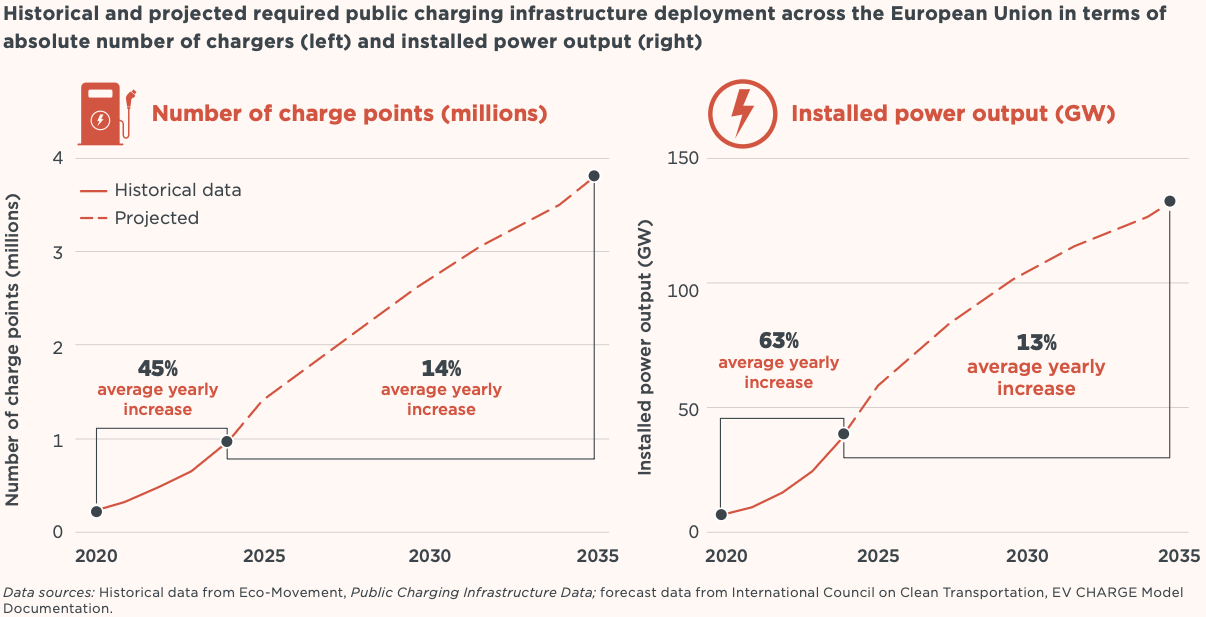

Global electric vehicle sales reached roughly 17 million in 2024, about one in every four new cars sold worldwide. China leads with nearly half of all new sales, Europe is stable around 25 percent, and the United States is catching up. This rapid adoption is reshaping how energy, real estate, and digital infrastructure interact.

Public charging capacity has also expanded quickly. Europe surpassed one million public chargers, while China hosts close to three million and continues to add high-power sites at a record pace. Yet headline figures hide the differences that matter: power per electric vehicle, grid access, and location quality determine how useful this infrastructure actually is.

For investors and founders, that means the growth story is still intact, but the value creation logic has changed. Expansion now depends less on installing more plugs and more on improving the economics of each site through data and software.

Sufficiency is local, and it defines the market thesis

There is no single formula for what “enough” charging looks like. It depends on how people live and move, on housing, commuting habits, and access to the grid. What’s sustainable in one market may look very different in another.

In suburban regions, home charging dominates because most drivers have private parking. In dense European cities, workplace and public fast charging are essential. Fleets and depots add another layer of complexity, requiring high uptime and predictable grid capacity.

For founders, this local variation defines product-market fit. Software that improves siting, forecasts utilization, or streamlines permitting can scale internationally because every market struggles with these same constraints in different ways. For investors, it separates scalable business models from those tied to local infrastructure economics.

The better metric is not chargers per vehicle — it is charging power, uptime, and profitability per driver. That is where planning intelligence, energy management, and operational excellence matter most.

The market is rewiring itself

Three structural shifts are changing where and how value is created across the charging ecosystem.

1. Regulation is forcing openness

In Europe, new rules such as the Alternative Fuels Infrastructure Regulation (AFIR) and the Data Act are making interoperability mandatory. Every public charger will need to support ad-hoc card payments and user-controlled data access. Closed systems are giving way to open networks and startups that make these transitions seamless will shape the next generation of infrastructure.

2. Capital is shifting

Large charge point operators are no longer venture companies. They are financed by infrastructure funds, utilities, and energy majors through green loans and project finance. This capital is suited for scaling networks but not for generating venture returns. The gap that opens is for software-driven companies that improve performance without heavy assets.

3. Profit pools are moving upstream

By the end of this decade, a significant share of charging profits will come from smart energy services such as tariff optimization, load balancing, and grid flexibility. Home and workplace chargers will dominate volume, but the highest margins will sit with digital and energy-integrated models.

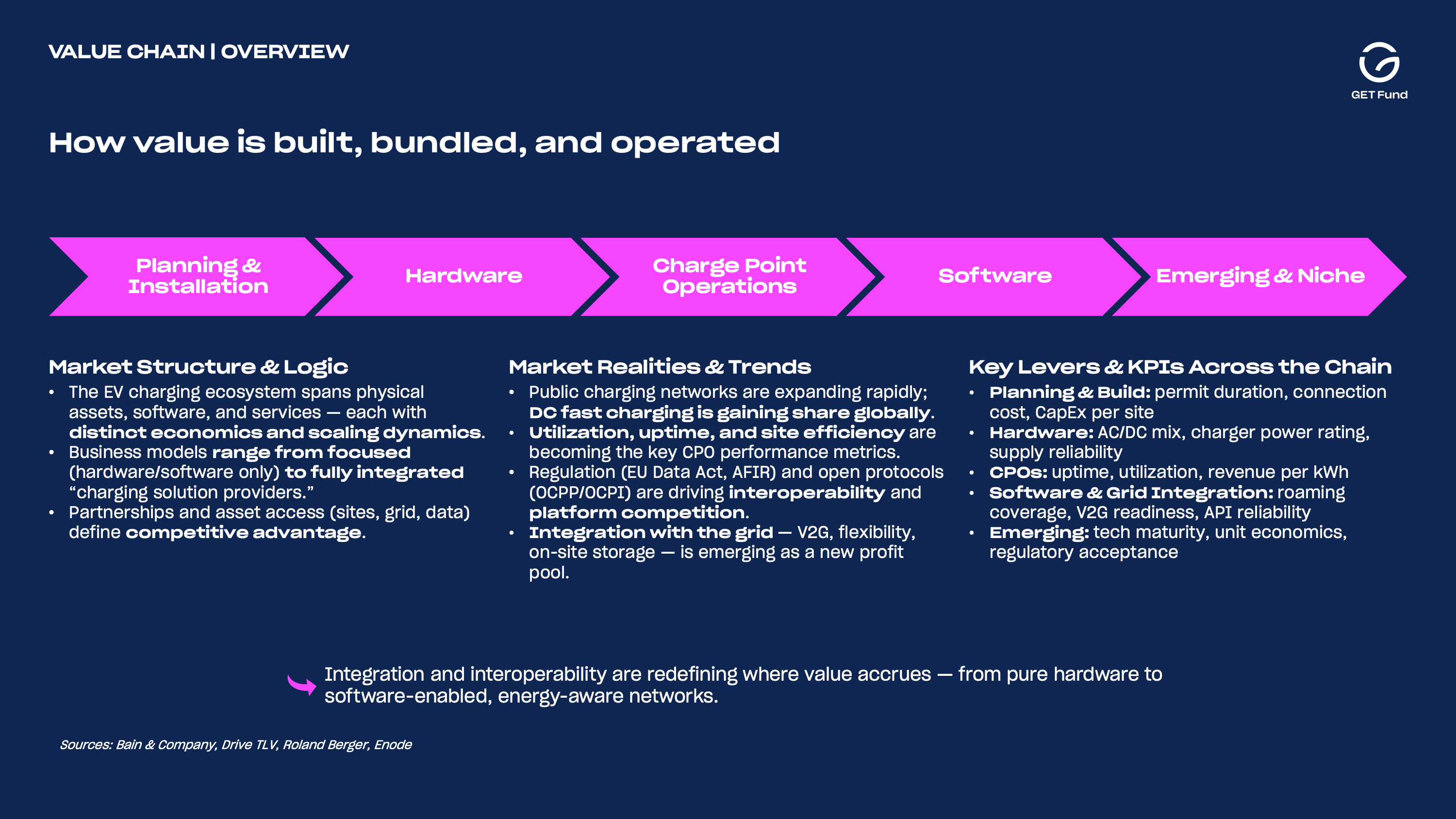

How value builds across the chain

The charging value chain used to be linear: plan, build, operate, maintain. It is now interconnected, with data and software linking every layer.

- Planning & Installation: Artificial intelligence siting, grid-capacity modeling, and streamlined permitting accelerate deployment, while efficient installation and predictive maintenance turn projects into reliable assets.

- Hardware: Reliability, serviceability, and open protocols drive purchasing decisions, with value shifting toward integrated software and service models.

- Charge Point Operations: Utilization, uptime, and energy optimization determine profitability, making operational data and dynamic pricing essential for achieving sustainable margins.

- Software: Payments, authentication, and interoperability software create recurring, asset-light revenue streams across networks and geographies.

- Emerging and Niche Technologies: Megawatt, robotic, and wireless charging solutions address specialized segments and signal the next wave of infrastructure innovation.

Each layer creates different kinds of opportunities. Some require capital discipline, others rely on network effects or product speed. What connects them is a shift from hardware differentiation to data-driven performance.

Where venture returns still live

- Interoperability and data platforms: Open standards are here, but implementation remains fragmented. Companies that unify billing, roaming, and data exchange across networks can scale rapidly through software economics.

- Flexibility and energy orchestration: Vehicle-to-grid aggregation, tariff optimization, and fleet-level energy management are turning charging infrastructure into an active part of the power system. These models generate recurring revenue that grows with electric vehicle adoption.

- Software for planning and reliability: Tools that predict grid capacity, model utilization, or enable proactive maintenance shorten development timelines and increase asset profitability.

- Integrated user experience: Account and payment systems that work across home, workplace, and transit charging create loyalty and simplify energy integration for drivers and fleets.

The simple rule is that hardware and operations consume most of the capital, while software, data, and flexibility services capture most of the margin.

The startup landscape

Europe’s startup landscape reflects this evolution. Hardware manufacturing and large network operations are consolidating under infrastructure investors. Meanwhile, new entrants focus on the digital and operational layers that make networks more profitable.

These companies do not need to own the chargers to create value. They make everyone’s chargers work better.

What we are watching

The next generation of winners in electric vehicle charging will not simply build faster. They will make the system smarter. They will connect mobility and energy, turning infrastructure into a platform for flexibility, resilience, and better economics.

If you are building technology that improves planning, operations, or energy integration for the charging ecosystem, we would like to hear from you.

Connect with us to explore how we can support your journey or pitch us your startup.

Back to Insights